Key points:

- A payroll budget covers more than salaries: the true cost of employment is 1.25 to 1.4 times base pay once employer NI, pensions, benefits, and admin costs are included.

- The 2025 Autumn Budget rewrote the numbers: employer NI rose to 15% and the secondary threshold halved to £5,000, making any pre-Budget payroll projections unreliable.

- Small errors compound fast: applying blanket percentage increases, missing April rate changes, and excluding payroll teams from planning are the most common culprits behind mid-year budget overruns.

- Building the budget is only half the job: a structured compensation review process is what turns a payroll budget into defensible, market-aligned salary decisions for every individual on your team.

Payroll is almost always the biggest line item on a company's budget. And after the 2025 Autumn Budget rewrote employer National Insurance rates and halved the secondary threshold, most payroll projections that you made for 2026 are likely already out of date.

But not to worry. That’s exactly what this guide is for. We’ll walk you through every employer-side cost you need to include in your budget, using current 2026/27 UK rates. We’ll run you through the steps needed, along with some mistakes that can muddy your forecasts if you’re not careful.

So, if you're an HR leader, Head of People, C&B Manager, or Finance Director at a company with 250 or more employees, you’re in the right place. We know how high-stakes payroll budgeting is, which is why we’re not going to whack you over the head with basic advice you might find in other articles.

So let’s get into it.

{{ ai }}

What is payroll budgeting?

A payroll budget is a financial forecast of all employer-side costs associated with your workforce over a set period, typically aligned with the UK tax year. That means gross wages, employer taxes, pensions, benefits, statutory payments, and administrative overheads. All of it, not just salaries.

Then came the 2025 Autumn Budget.

Employer NI jumped from 13.8% to 15%, and the secondary threshold – the point at which NI kicks in – was halved from £9,100 to £5,000. Payroll.org described it as "one of the most payroll-centric packages in years." If your projections predate that announcement, they need revisiting.

Now, while payroll budgeting does help you keep on the right side of HMRC, it can also provide more benefits than simple regulatory compliance. Done well, it gives you:

- Forecasting accuracy across your largest cost line.

- A defensible basis for headcount decisions when the CFO asks questions.

- A framework for aligning compensation spend with actual business goals.

It’s a strategic tool for your organisation, and one that allows both finance and HR to sing from the same hymn sheet throughout the year.

Every cost that belongs in a payroll budget

The true cost of employing someone is estimated to run at 1.25 to 1.4 times their base salary. The gross wage on the contract is just the starting point.

Here's what the full picture looks like at current 2026/27 UK rates:

Wages

Start with gross wages. This is the salaries for salaried staff, and hours multiplied by the hourly rate for workers. It’s your baseline, without the additional bells and whistles that make up your budget.

While it is the baseline, there are a couple of points that can cause some confusion:

- PAYE is not an employer cost: income tax is deducted from the employee's salary and remitted to HMRC by the employer. It doesn't add to your payroll budget. It's simply withheld on the employee's behalf. You'll see it listed as an employer expense on some guides, but that's incorrect.

- Holiday pay doesn't inflate your budget either: employees are paid at their full rate during leave, so it's already captured in gross wages. No need to add a separate line.

Employer National Insurance

Employer Class 1 NI sits at 15% on earnings above £5,000 per year (the secondary threshold) for 2026/27. This is up from 13.8%, with the threshold previously at £9,100.

💡 The Employment Allowance rose to £10,500 for 2026/27, and the previous £100k NI liability cap was removed. That means most private-sector employers now qualify. There is one exception, being single-director companies with no other employees.

A few things to keep in mind when building your budget:

- Class 1A NI on benefits in kind also sits at 15%.

- Calculate NI per employee rather than applying a flat rate across all staff, though individual circumstances vary.

- Factor in the Employment Allowance before finalising your NI total.

Pensions, benefits, and Apprenticeship Levy

We’ll start off with auto-enrolment pension. The minimum employer contribution is 3% on qualifying earnings between £6,240 and £50,270 for 2026/27. The earnings trigger sits at £10,000 per year, a threshold the government maintains for what it calls "policy stability."

A few things to watch here:

- Calculate per employee, not as a flat 3% of total payroll. Some staff opt out, and many employers contribute above the minimum.

- Salary sacrifice for pension contributions saves the employer NI on the sacrificed amount.

- Benefits in kind (private health insurance, company cars, cycle-to-work schemes) attract Class 1A NI at 15% on top of their direct cost.

Apprenticeship Levy: If your annual pay bill exceeds £3m, add 0.5% of your total pay bill. The £15,000 allowance still applies, so factor that in before calculating your liability.

Overtime, bonuses, and commissions

These are the hardest line items to forecast and the ones most likely to cause a mid-year headache if you've underestimated them.

The most reliable approach is to use previous years' data as a baseline, with a ±10% variance assumption built in.

Some concrete examples of what that looks like in practice:

- If a salesperson typically earns 50% commission on base, budget on that same assumption.

- If your team logged 100 hours of overtime last August due to seasonal demand, project month by month rather than spreading an annual average evenly across the year.

This is the forecasting section, because you’re never going to have all these numbers on hand. You just need to account for them in your budget (through historical analysis), but there’s no guarantee that you pay specific bonuses, or that overtime will be as high… the only issue is that it can easily go the other way, too.

Statutory payments and admin costs

These line items are commonly left out of payroll budgets. They shouldn't be.

Statutory payments – maternity, paternity, adoption, and sick pay – are employer obligations. They're hard to predict with precision, but you can use historical payroll records to estimate likely spend and set aside a contingency for the rest.

Admin costs to include:

- Payroll software subscriptions (which often scale with headcount).

- Recruitment and agency fees.

- Outsourced payroll provider fees.

- Employment liability insurance.

None of these is glamorous. But they're real costs of maintaining a workforce, and leaving them out means your budget will always come up short.

How to build your payroll budget

Now that’s out of the way, we can actually get onto how to build your payroll budget. We’ll run you through each step, including the data you need to be working with and the calculations you need to make. Let’s start with the old HRIS pull.

Step 1: Gather current headcount and employment data

Before any calculations happen, you need clean data.

Pull each employee's gross salary (or hourly rate and contracted hours), employment type, and location from your HRIS. This sounds straightforward, but it's worth being thorough – outdated or incomplete records at this stage will create inaccurate budget figures downstream, and you won't always spot the error until it's too late.

Step 2: Calculate the full employer cost per person

This is where you’re going to use that 1.2 to 1.4 multiplier from earlier.

For each employee, apply every component from the previous section: gross wage + employer NI + pension contribution + benefits in kind + a share of statutory provisions.

To make that concrete: an employee on £45,000 gross adds roughly £6,000 in employer NI and approximately £1,163 in minimum pension contributions. All before you've added any benefits. That's close to £52,000 in total employer cost for someone earning £45k on paper.

‼️Many budget overruns happen at this exact step. Not because anything went wrong, but because teams forgot to include the full employer cost and only budgeted for gross salary.

Step 3: Aggregate by department or cost centre

Once you have individual costs calculated, group them by department or cost centre.

This step is less about maths and more about visibility. Budget owners need to see which teams are driving the largest share of payroll spend, and that's much harder to act on if everything sits in one undifferentiated total. Breaking it down also makes it easier to have productive conversations with department heads during the planning process.

Step 4: Layer in planned changes

A payroll budget that only reflects your current headcount is already out of date.

Add confirmed new hires at full employer cost (not just salary), remove confirmed departures, and adjust for promotions and internal transfers.

Critically, account for timing: a September hire only costs four months of the budget year. Spreading their annual cost evenly across 12 months will overstate your spend and make your budget harder to reconcile with actuals later.

Step 5: Project salary increases using market data

This is where good data earns its keep.

Figures recommend breaking the salary increase budget into four distinct components: general increases, merit or promotion increases, inflation adjustments, and market adjustments. Treating these as one blended number tends to obscure where the money is actually going.

For benchmarks: WorldatWork's 2025–2026 survey – which covered 1,773 organisations across 22 countries – projects UK 2026 increases at a mean of 3.8%. That's a useful reference point, but the most accurate budgets are built on current market data, not last year's annual survey figures.

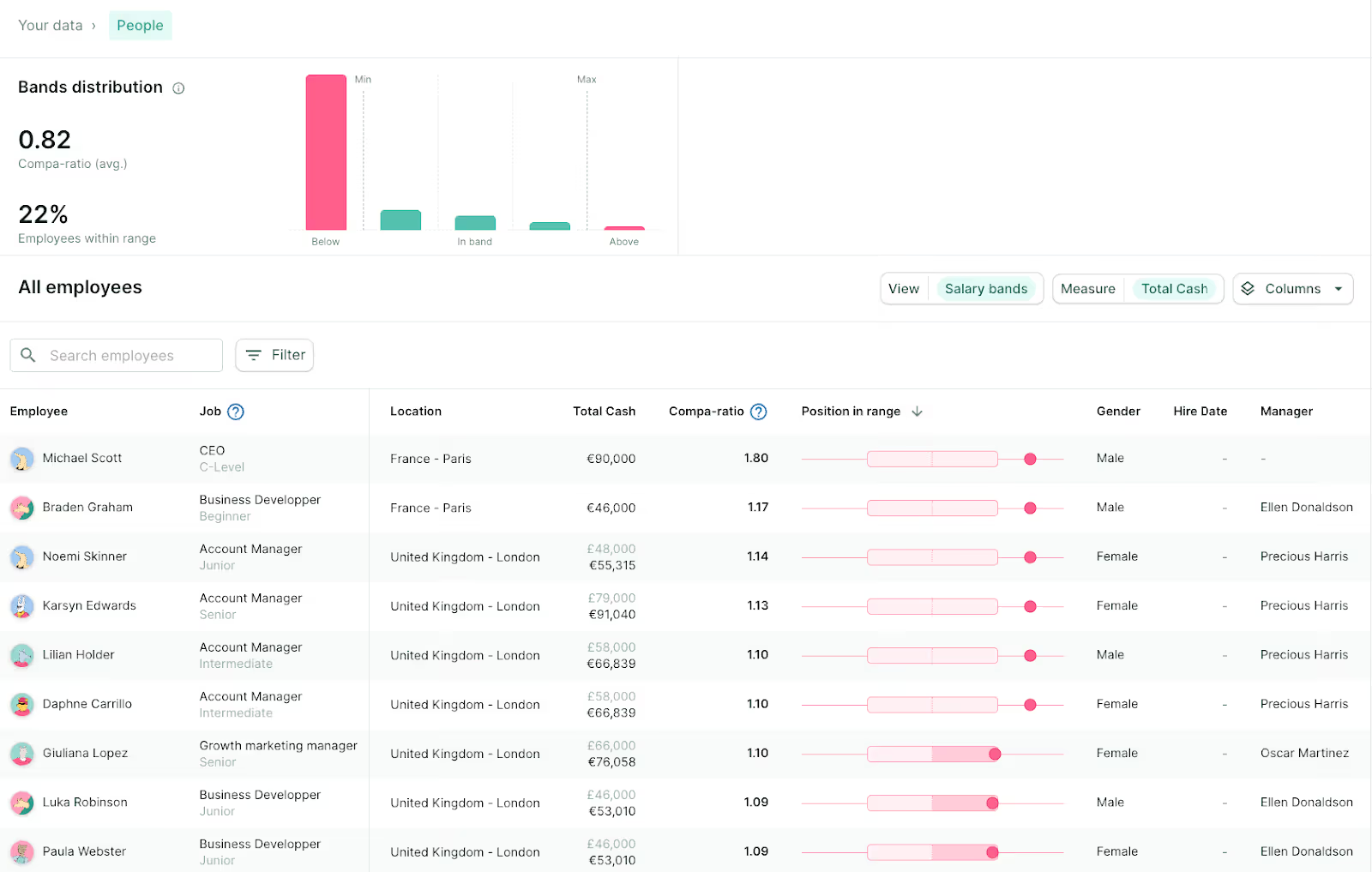

🤔 Figures is now powered by Mercer, providing international salary coverage across 3.5 million datapoints. On the Figures dashboard, you can easily check whether your employees sit within competitive salary bands for their roles, allowing you to set aside cash for salary increases in your budget for those sitting outside of salary benchmarks.

{{ cta }}

Step 6: Add variable cost estimates and a contingency buffer

Layer in overtime, bonuses, and commissions using the historical patterns you identified in Step 1, with a ±10% variance assumption.

Then add a contingency line. Rather than a pessimistic strategy that assumes you’ll overrun your budget, this is simply good planning.

Use it to absorb unknowns: statutory pay obligations that arise mid-year, regulatory changes, or unplanned turnover that triggers recruitment and onboarding costs. The size of this buffer will depend on your organisation's history, but having it at all puts you in a much stronger position than teams that don't.

Step 7: Sense-check with the payroll-to-revenue ratio

Once everything is aggregated, divide your total payroll costs by revenue.

For most businesses, a healthy range sits between 15% and 30%. In service-heavy sectors, that can climb above 50%. In highly automated industries, it may sit well below 15%. The specific number matters less than tracking your own ratio over time — if it's drifting upward year on year without a clear reason, that's worth investigating.

🤔 Notice the pattern there? Generally, higher payroll-to-revenue ratios relate to how crucial human labour is to the cash rolling into your business. Service industries where workers are essentially a selling point will have higher ratios than highly automated industries.

Step 8: Set a review schedule

Building the budget is only half the job. The other half is keeping it accurate.

Only 25% of payroll departments operate at optimised, strategic levels, according to HR.com. For companies with 250 or more employees, quarterly reviews are the minimum. For organisations with high workforce volatility, where frequent hiring, restructuring, or significant variable pay are a common occurrence, monthly rolling forecasts will give you far more control.

Set a calendar reminder for every April to update your statutory rates: employer NI, the National Living Wage, pension qualifying earnings bands, and the Employment Allowance. These change annually, and missing them is one of the most common — and most avoidable — budgeting mistakes around. Speaking of mistakes…

Common payroll budgeting mistakes

Even experienced finance and HR teams make these. Here's what to watch out for.

- Treating gross salary as total cost: employer costs run 1.25–1.4x base salary once NI, pensions, and benefits are factored in. Budgeting on gross salary alone guarantees a shortfall.

- Confusing employee deductions with employer costs: PAYE is withheld from the employee's salary. It's not an additional cost to you as the employer. Including it as a budget line will overstate your spend.

- Applying blanket percentage increases instead of using market data: incremental budgeting — last year's number plus X% — carries forward past inefficiencies without questioning them. Justifying each salary adjustment against current market data produces more accurate budgets and better decisions.

- Excluding payroll teams from the process: payroll specialists are often the first to spot overtime spikes, turnover patterns, and incoming statutory changes. Leaving them out of the planning process means missing insights that are sitting right there.

- Ignoring statutory rate changes until they hit: build an April calendar reminder to update employer NI rate and secondary threshold, National Living Wage, pension qualifying earnings band, and Employment Allowance.

The good news is that all of these mistakes are easily avoidable. We’ve already given you everything you need to ensure you don’t stumble into these pitfalls. Just ensure you’re working with good data and aren’t perpetuating last year's mistakes, keep up to date with changes, and know exactly what you need to include in your budget!

Putting your payroll budget to work

Your payroll budget sets the total envelope for compensation spend. The next step is deciding how to distribute it across individuals, which is where a structured compensation review comes in.

The two processes are inseparable. A budget without a disciplined review process is just a number. A review process without a live budget is a recipe for overruns.

Figures' compensation review module connects both. It provides monthly-updated Mercer benchmark data covering 3.5 million+ data points, real-time budget tracking as managers make recommendations, and multi-budget campaign management so you can handle merit increases, market adjustments, and promotions separately. All within a single review cycle.

Every salary decision is grounded in current market data, and your budget stays visible and under control from start to finish.

Want to see how it works in practice? Book a free demo with Figures, and we'll walk you through it.

Summarize this article with AI

No time to read it all? Get a clear, structured, and actionable summary in one click.